SpaceX, OpenAI, and Anthropic Are Going Public…Here's What Every Investor Should Know Before Buying a Share.

Brian Seay, CFA | Capital Stewards

The IPO calendar for the summer of 2026 is stacked. SpaceX is likely to go public later this week, Anthropic filed to begin the process a few weeks ago and OpenAI kicked off their process formally today. The excitement is real. So is the risk.

In our experience serving clients across Alabama, Georgia, and Tennessee, the moments of greatest investment opportunity are also the moments of greatest investment peril. IPO season has a way of making people feel like they're missing something if they don't act — and that feeling has cost investors dearly before.

In this piece, we'll walk through how IPOs actually work, what we know about each of these three companies, how to think about their investment merit, and what history tells us about buying into the hottest IPOs of any given era. Our goal, as always, is to help you be a good steward of your resources — not just to participate in the excitement.

How an IPO Actually Works

Most investors have a general sense that an IPO is when a company "goes public," but the mechanics behind that process matter enormously for understanding what you're actually buying.

When a company decides to pursue an IPO, it typically begins by hiring investment banks — called underwriters — to manage the offering. These banks help the company prepare a registration statement, known as an S-1, which is filed with the Securities and Exchange Commission (SEC). The S-1 is the first time the public gets to see a company's full financial picture: revenue, expenses, debt, risks, and the story management is telling about the future. Companies initial file a “confidential” version of this document with the SEC for review. However, even though the initial document isn’t public, many companies announce they filed to begin building demand for their shares.

After the SEC reviews the filing, the company and its bankers embark on a roadshow — a series of presentations to institutional investors like mutual funds, pension funds, and hedge funds. Based on the conversations with potential investors during those meeting, the bankers (known as underwriters) help set an IPO price. This is an important part of the process because it allows the company and potential investors to work together on a fair price for their shares, a price where the demand for shares will somewhat match the initial supply.

The night before the IPO, the banks collect cash from investors in exchange for shares at the IPO price. In order to buy shares at the IPO price, investors must work with their broker, like Morgan Stanley, Goldman Sachs, Fidelity or Charles Schwab, to obtain an “allocation” of shares in the initial sale. Generally, demand is above supply, so investors may ask for say 1,000 shares but they might only receive 100. One thing you might see is that an IPO is “oversubscribed,” meaning more investors want to buy shares than there are shares to sell. A word of caution here though, because many investors don’t receive the shares they ask for, they inflate their ask to the banks. That means for an IPO to be successful, you really want to see it many times oversubscribed, say 7-10x. Not just 1-2x to ensure there is really enough demand to support the stock when it starts trading.

The next day, typically during the middle of the day, the shares begin trading on an exchange, that's the IPO day. A “good” result on IPO day is generally when a stock trades 5-10% higher. That means the investors that bought the shares are happy with their investment and the company owners didn’t sell at too low a price.

Here's the part most retail investors don't realize: If you don’t receive an initial allocation before trading, by the time you can buy shares on your brokerage app the shares have likely already started moving up or down, perhaps significantly. So it’s important to be thoughtful about requesting shares ahead of time if you want to own the company initially.

The Three IPOs to Watch: What We Know

SpaceX — The Rocket That's Already on the Launchpad

SpaceX is the furthest along of the three. The company filed a confidential S-1 with the SEC in April 2026, made it public in May, and has set an IPO price of $135 per share — targeting a valuation of approximately $1.77 trillion. Goldman Sachs is leading a 21-bank underwriting syndicate, and the roadshow began around June 4 and the shares are expected to begin trading this Friday.

The financial picture is genuinely impressive in some respects. SpaceX reported $18.7 billion in total revenue for 2025, a 33% increase over the prior year. Starlink, its satellite internet service, contributed $11.4 billion of that total. The company ended 2025 with $24.7 billion in cash on hand — a meaningful cushion.

But profitability is another story. SpaceX posted a net loss of $4.9 billion for the year, driven by heavy investment in Starship development, satellite expansion, and AI data centers following its 2026 acquisition of Elon Musk's xAI subsidiary. Its “Connectivity” business, essentially Starlink, generated about $7 billion in adjusted EBITDA, a proxy for cash flow, and the company used all of that profit plus more to invest in its space and AI businesses.

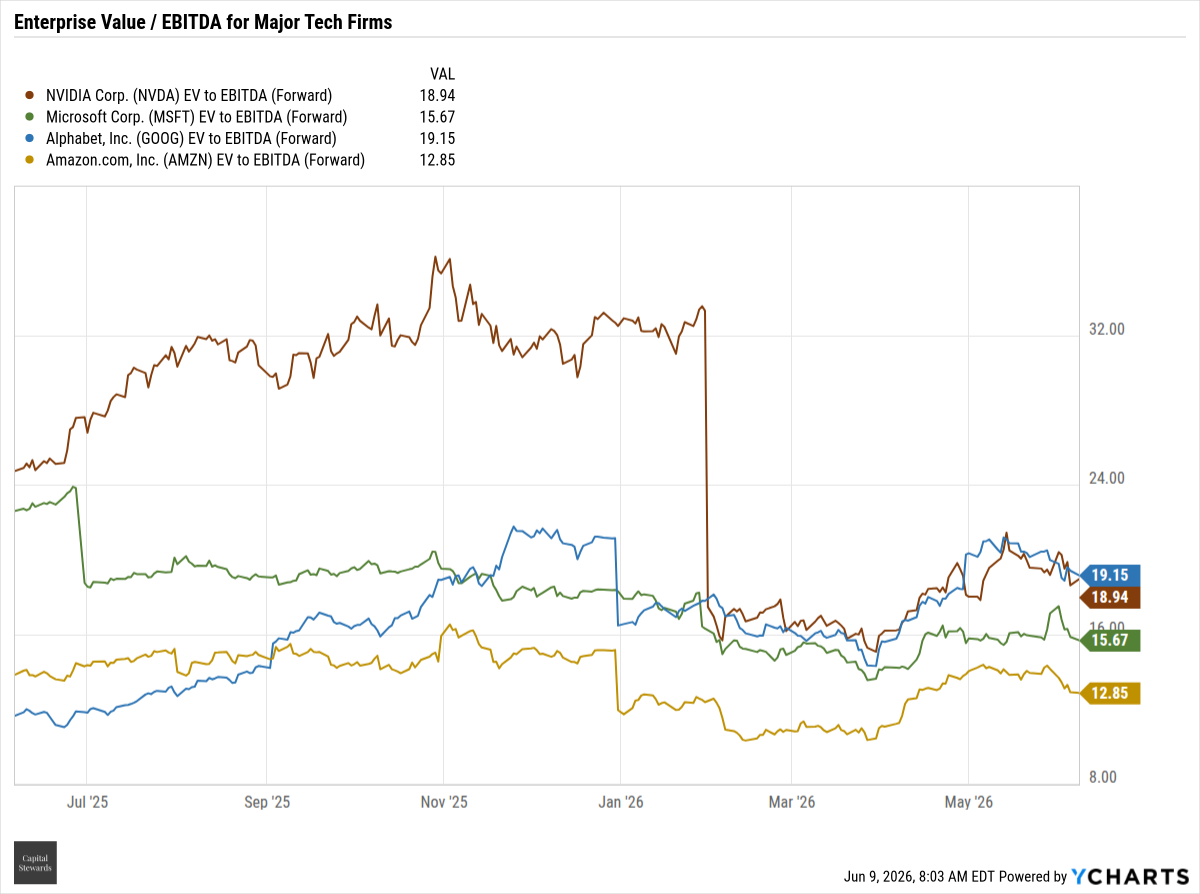

My own view is the way to value the whole business is to think about what the value of the connectivity business would be if it stood alone, since it’s the only current cash flow generation segment of the business. The connectivity business has real value today and then the others are like moonshots, or options that you hope pay off long term. If you assume EBITDA from Starlink grew 100% - or doubled – each year for the next 3 years, that business would be generating about $56 billion in EBITDA. That means, $14 billion in 2026, $28 billion in 2027 and $56 billion by say the end of 2028, the business would be worth 31x EBITDA in 2028. For reference, Google, Microsoft and Nvidia trade between 14 and 16 times EBITDA today. So for Spacex to be “worth it,” you need to have some pretty lofty beliefs about its ability to grow cash flow from its connectivity business and also become profitable in its Space and AI segments.

The other wrinkle with the SpaceX IPO is that Elon and SpaceX essentially set the price at $135 per share ahead of time, without going through the price discovery conversations that occur during the roadshow. So investors will need to decide if they are in or out, and the real “price discovery” will happen when the stock begins trading. That means the first day is likely to be even more volatile than the typical IPO as the price could move up or down wildly as the market determines whether $135 is fair or not.

OpenAI — The Most Valuable Brand in AI, Still Looking for Profit

OpenAI filed its S-1 recently as well. The company completed a major restructuring in October 2025, transitioning from its unusual nonprofit-capped-profit hybrid structure to a public benefit corporation — a necessary step before any IPO could proceed.

The revenue growth at OpenAI is staggering. The company went from roughly $2 billion in annualized revenue at the end of 2023 to over $20 billion by the end of 2025. ChatGPT has approximately 900 million weekly active users, making it one of the fastest-adopted consumer technology products in history. A $122 billion private funding round in March 2026 valued the company at approximately $852 billion.

The concerns are equally significant. OpenAI is deeply unprofitable. According to media interviews with executives, the company lost $9 billion in 2025 and expects to lose almost $74 billion in 2028 before seeking to generate profits in the early 2030s.

There is also the structural complexity of Microsoft's position. After investing $13 billion, Microsoft holds approximately 27% of OpenAI PBC and has a $250 billion Azure services commitment with the company. Understanding how that relationship affects the economics available to public shareholders is a question that will require careful reading of the S-1 when it arrives.

Anthropic — The Enterprise Bet on Safe AI

Anthropic made history on June 1, 2026, when it confidentially filed a draft registration statement on Form S-1 with the SEC — meaning this company may move from confidential to public filing before the end of the summer. Anthropic recently closed a private round of funding at a valuation of $965 billion, implying an IPO valuation of more than $1 Trillion like SpaceX.

Anthropic's financial trajectory is remarkable. Media outlets are reporting revenue near $50 billion as of late May 2026 — driven primarily by enterprise adoption and the rapid growth of Claude Code. Different than OpenAI and SpaceX, Anthropic projects positive cash flow by 2027–2028.

What distinguishes Anthropic from OpenAI in the investor calculus is its business mix. Approximately 80% of Anthropic's revenue comes from enterprise customers, compared to roughly 40% for OpenAI. Enterprise revenue is generally more predictable, more defensible, and more aligned with sustainable pricing power. A study from the business expense management software company known as Ramp showed that Anthropic’s customer base has grown from 9% of Ramp customers to 34% in the last year.

The risks are real here too. Anthropic has massive compute commitments — including arrangements with AWS, Google, Microsoft Azure, and SpaceX — that total tens of billions of dollars over the next several years. The company will need continued explosive revenue growth to service those commitments and reach profitability. And as a company with a declared safety-first mission. It’s likely that its “safety approach” cost it billions in defense department contracts earlier this year. Anthropic will need to demonstrate that safety and commercial growth are not in tension

What History Teaches Us About IPOs

IPOs That Created Generational Wealth

The most important lesson on IPOs is that trading the day of the IPO is more akin to gambling than investing. Amazon, Microsoft and Nvidia all saw significant gains the day of their IPO. Google and Meta (facebook at the time), did not. What these winners all share: a genuine and durable competitive advantage, a large and expanding addressable market, and a business model that was capable of generating real cash flow at scale — even if it took years to prove it. The real returns in all of these names happened years – really more than a decade - after the IPO. Yes, if you held the stock from the IPO onward, you would have been rewarded, but investors that invested later could still have made significant returns in any of those companies.

Amazon (1997): Amazon went public at $18 per share with a market cap of roughly $438 million. The company lost money for years and was widely mocked as "Amazon.bomb" during the dot-com bust. Investors who held through the skepticism — or bought after the crash — were eventually rewarded with one of the greatest returns in stock market history.

Apple (1980): Apple's IPO generated enormous investor interest from day one, but the real story is the long-term compounding for those who held through multiple near-death experiences, including Steve Jobs's ouster in 1985. The lesson is less about the IPO and more about holding a genuinely exceptional business through adversity.

Google (2004): Google's IPO was managed by Wilson Sonsini — the same law firm Anthropic has retained for its own public offering — using a novel Dutch auction structure designed to give retail investors more equal access. The stock opened around $100 and has since risen many times over. But even Google had meaningful early volatility that tested investor conviction.

When the Hype Crushed the Returns: Meta's IPO

Meta (then Facebook) went public on May 18, 2012, at $38 per share — valuing the company at approximately $104 billion. It was the most anticipated IPO since Google, and the excitement was overwhelming. Retail investors lined up to get shares. Business anchors talked about generational wealth creation occurring on the back of the IPO.

Within three months, the stock had fallen to $18 — a 53% decline. Within a year, it was still trading below $30. The problem was not that Facebook was a bad business. It wasn't. The problem was that investors paid a price that had already baked in years of optimistic growth assumptions. The company was also navigating a critical transition — desktop advertising revenue was strong, but mobile monetization was unproven in 2012.

Meta eventually became one of the most profitable businesses in American history, and those who bought at the $38 IPO price and held were ultimately rewarded. But that required holding through a painful 53% decline and years of uncertainty. Investors who bought at the IPO high and sold at the low locked in real losses.

The lesson from Meta is not that great companies make bad IPO investments. It is that even great companies can be overpriced at the moment of maximum excitement — and that retail investors who buy into the hype rather than the fundamentals often end up holding the bag.

How to Think About These Investments as a Long-Term Steward

Valuation Is Not a Technicality — It's Everything

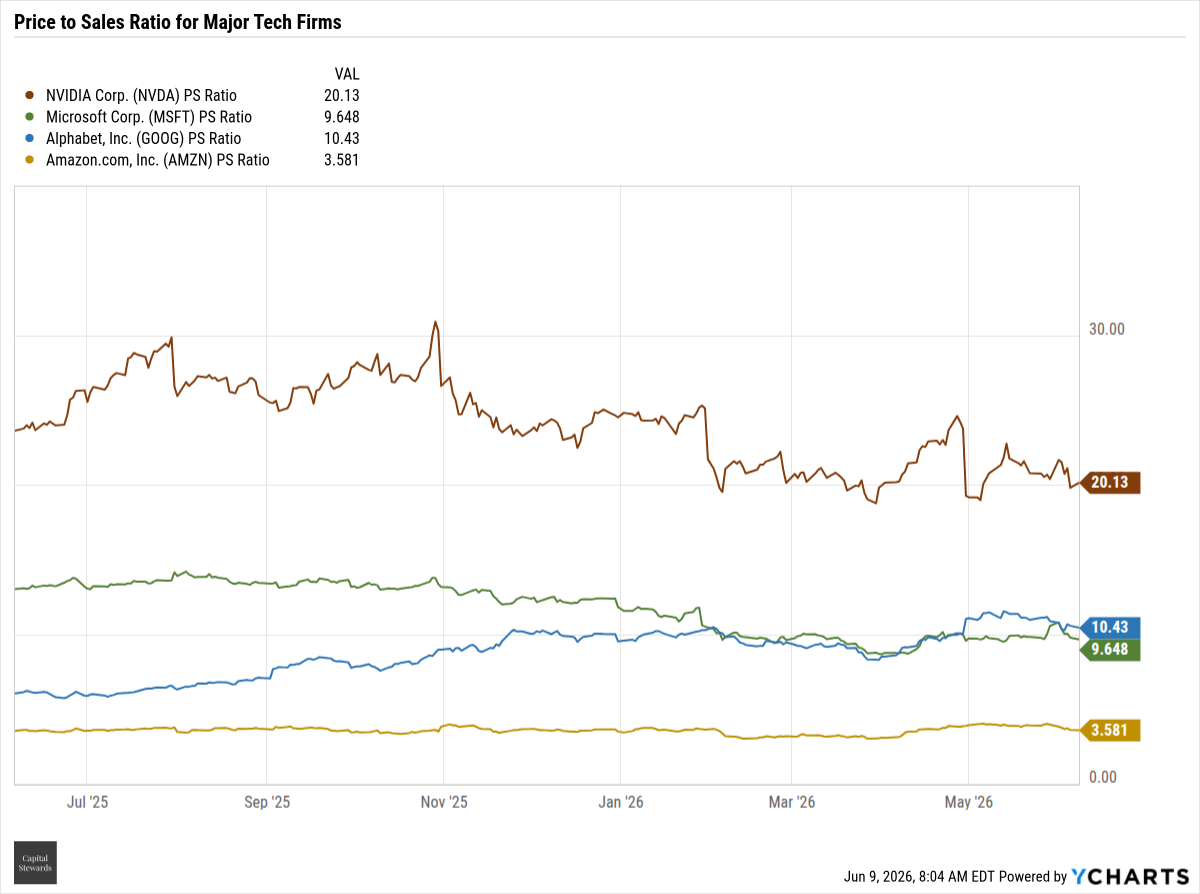

At a reported $1.77 trillion valuation, SpaceX would be priced at roughly 95 times its 2025 revenue. At $852 billion, OpenAI is priced at approximately 65 times 2025 revenue. Anthropic would represent a similarly elevated multiple. For context, Alphabet — one of the most profitable and dominant technology companies in history — trades at roughly 10 times revenue. Microsoft also trades around 10x revenue. Lofty Nvidia trades at 20x revenue.

These multiples are not automatically wrong. Fast-growing, capital-light businesses with network effects and durable competitive advantages can justify elevated revenue multiples. But they do require everything to go right: sustained revenue growth, improving margins, no major competitive disruption, and continued investor appetite for unprofitable growth stories. That's a long list of conditions.

Profitability Matters More Than Excitement

All three of these companies are currently unprofitable — or, in SpaceX's case, profitable in some segments and deeply unprofitable in others. That's not unusual for high-growth companies, and it doesn't make them uninvestable. But it means you are being asked to pay for a future that hasn't arrived yet.

The key question is: what does the path to profitability look like, and how certain is it? Anthropic, with its enterprise-heavy model and projected positive cash flow by 2027–2028, has perhaps the clearest near-term line to sustainable economics. OpenAI's path requires resolving several structural questions — the Microsoft partnership economics, the competitive pressure from Google and Anthropic, and the sheer scale of compute spending required to stay at the frontier.

Governance and Control Are Non-Negotiable Due Diligence Items

Elon Musk will retain dominant voting control over SpaceX through a multi-class share structure. That means public shareholders will own economic exposure but limited governance influence. This is a feature many Silicon Valley founders insist upon, and it has worked well in companies like Alphabet and Meta — until it hasn't. Understanding what you're actually purchasing is essential.

OpenAI's transition from nonprofit to public benefit corporation is unique and legally complex. The nonprofit foundation retains a 26% stake in the new PBC, and the mission language around artificial general intelligence creates governance dynamics that have no clear precedent in public markets. Read the S-1 carefully on this point.

Concentration Risk and Position Sizing

For most individual investors, the right question is not whether SpaceX or OpenAI is a good business. It probably is. The right question is: how much of my retirement security should be concentrated in a single pre-profit technology company, purchased at the moment of maximum public excitement?

A speculative position — say, one to two percent of a well-diversified portfolio — allows you to participate in the upside without catastrophic consequences if the valuation corrects. Concentrating five, ten, or twenty percent of your investable assets in any single IPO story, no matter how compelling, is not investing wisely. It is speculation with resources that belong to your future.

Lockups and Index Inclusion

When insiders — employees, venture capital firms, and early investors — receive their shares at IPO, they are typically subject to a 180-day lock-up period during which they cannot sell. When that window expires, a wave of selling often follows. This is one reason why some of the best IPO entry points come six to twelve months after a listing, when the lock-up expiration has passed and early investors who want liquidity have already sold.

This year, the Nasdaq will more quickly than usual to include SpaceX and presumably Anthropic and OpenAI into its top 100 index, otherwise known by the ticket QQQ or the Qs. That will create automatic demand for the shares of the company, likely around $20 Billion or so. But, before you think that the index demand will drive the price up on its own, these stocks are very liquid. Nvidia regularly sees more than 150 million shares trade on a single day, representing more than $31 billion in value. So the index demand will help, but its not going to cure everything if the underlying demand for the shares is not strong. Not to mention hedge funds front run index buying, which helps offset price movements in the market when the index’s rebalance and buy shares.

Patience is a competitive advantage in IPO investing. The institutional investors who got shares at the offering price will often use early retail enthusiasm to distribute shares at a profit. Waiting for the dust to settle is not the same as missing the opportunity.

Questions Worth Asking Before You Buy

If you are considering a position in any of these companies after they list, here are the questions we would encourage you to work through:

What am I actually buying? Read the S-1. Understand the share class structure, the governance rights, the key risks the company itself has disclosed, and the competitive landscape.

What price does this investment require the company to achieve, and over what time horizon? Work backward from the valuation to understand what growth rate, margin profile, and market share capture would be necessary to earn a reasonable return.

How does this fit within my overall financial plan? Is this money I can afford to lose entirely if the valuation corrects by 50% or more? If not, the position is too large.

Am I buying because of the business fundamentals, or because I'm afraid of missing out? Fear of missing out is one of the most expensive emotions in investing.

What is my time horizon and exit plan? A speculative position with no plan is a recipe for selling at the worst possible time under emotional pressure.

Have I considered the tax implications? IPO investing, especially short-term, can generate short-term capital gains taxed at ordinary income rates.

The Bottom Line

SpaceX, OpenAI, and Anthropic represent three of the most consequential technology companies in modern history. The underlying technologies — reusable rockets, frontier AI models, satellite internet — have genuine transformative potential. These are not frauds or empty hype machines.

But good companies and good investments are not the same thing. The price you pay matters enormously. And the history of high-profile IPOs — from the Meta disappointment to the Amazon triumph — suggests that the best long-term investors are the ones who do the hard work of valuation, exercise patience, size positions appropriately, and refuse to let excitement crowd out discipline.

At Capital Stewards, our job is to help you think through exactly these kinds of decisions — not just whether a company is exciting, but whether a particular investment, at a particular price, makes sense in the context of your specific financial goals and values. If you want to talk through how these IPOs fit — or don't fit — into your plan, we'd welcome that conversation.

Stewardship doesn't mean sitting on the sidelines. It means being intentional about risk, valuation, and the purpose behind every investment decision. The best stewards don't chase headlines — they build portfolios that endure.